Snap: Increasingly Asymmetric.

Q2 2025 ER Digest

With over 350M AR (augmented reality) DAUs (daily active users) I believe that Snap’s differentiated user experience philosophy positions them for a bright future, as AR technologies go mainstream.

And trading at just over 2 times sales, I view Snap as an increasingly asymmetric pick. The market has left Snap for dead, but fundamentals point to a strong company.

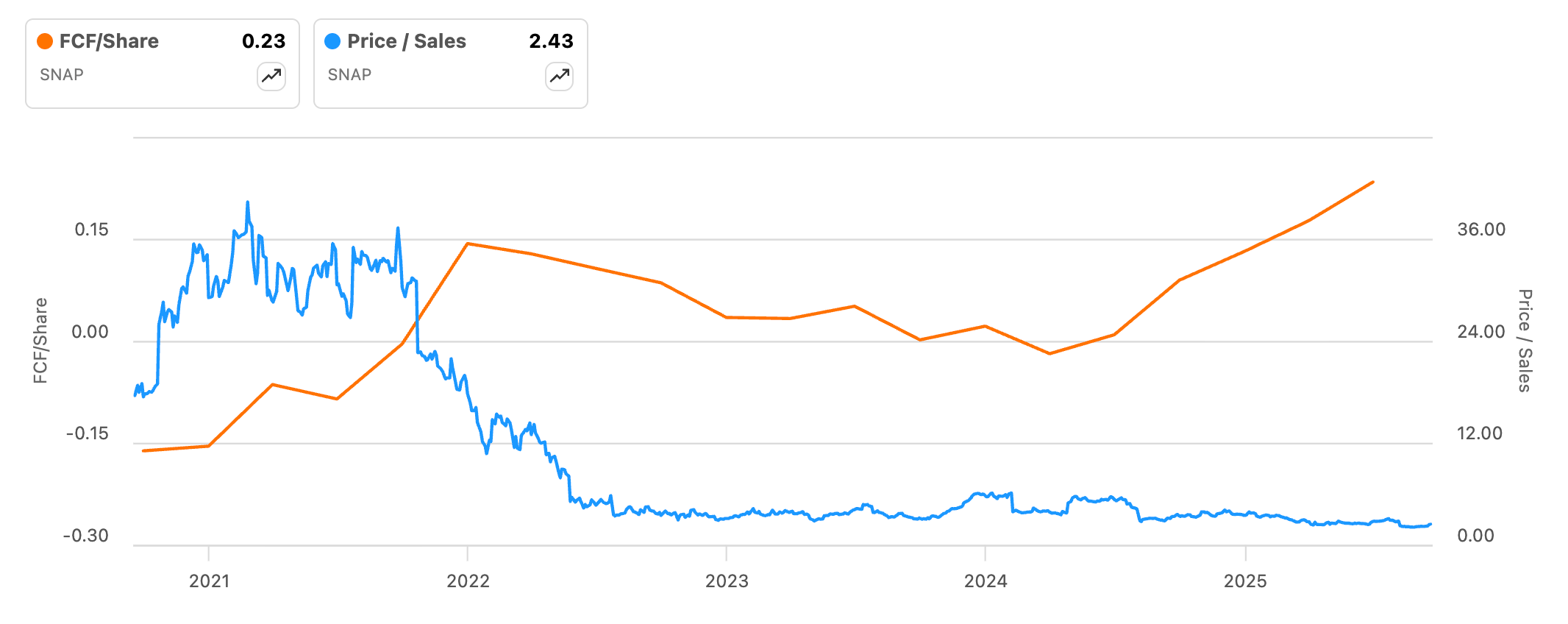

Snapchat’s stock price continues to diverge from fundamentals, as evidenced by the graph below. Free cash flow per share (orange line, left axis) is rising speedily and the stock is trading at just over 2 times sales (blue line, right axis), with Snap thus presenting an increasingly asymmetric investment opportunity. Since I wrote my original Snap deep dive, I’ve noticed many individuals from a long list of nationalities using Snap in all kinds of settings. Indeed, while the prevailing narrative is that Snap is an irrelevant social media network, it’s actually one of the most prevalent ones on Earth with 932M MAUs as of Q2 2025, up from 900M in Q1 2025. Additionally:

The rising free cash flow per share demonstrates Snap’s ability to monetise. The focus on improving monetisation is palpable throughout Snap’s earnings calls.

Simultaneously, Snap is growing new verticals well, which demonstrates an ability to enhance engagement over time.

For example, Snapchat+ subscribers are up from 15M to 16M QoQ, with annual revenue run rate increasing from $600M to $700M QoQ. In turn, 175M MAUs now play games on Snap, up 40% YoY, which is a rather striking increase. As additional examples, time spent on Snap’s Spotlight (a short-form, TikTok-style video platform) is up 23% YoY, now making up for 48% of total time spent on Snap. Further, Snapchatters now spend 30% more time video chatting than they did a year ago. With a solid track record of increasing engagement and monetising it, I’m increasingly confident about Snap’s ability to create value long term.

Over time, I’ve also come to understand that Snap’s moat is its unique focus on enabling you to interact with friends in the world, which sets Snap up for an appealing future in the realm of AR (augmented reality). While it’s questionable whether Snap’s vertically integrated AR infrastructure does present a moat relative to Meta, for example, I’m increasingly convinced of the value of Snap’s proprietary data, since it emerges from a completely different user experience philosophy. As of Q2 2025, Snap had over 350M augmented reality DAUs (daily active users), which really puts the following remarks by Snap CEO Evan Spiegel during the Q2 2025 earnings call into context:

[Prepared remarks]: Enriching relationships between friends and family is central to our mission, and we continue to build products that bring people together and spark conversations among Snapchatters from messaging and maps to personalised content and AR experiences.

[Prepared remarks]: We have made a long-term and consistent investment in augmented reality, committing more than $3 billion over the past 11 years to develop the world's only full stack vertically integrated, augmented reality platform.

[…]

[Q&A section]: We're incredibly passionate about the opportunity to reinvent the computer. People are spending more than 7 hours a day now, on average, staring down screens. And I think even just moving a couple of hours of that to looking out at the world through see-through lenses and a pair of glasses can make a meaningful difference for people's well-being, but also the way they interact with computing and in AI in general.

So the opportunity is enormous. Obviously, this is a space we've been committed to.

Actually, since before Snapchat had chat, so more than, I guess, 11 years now. And I think really fortunately, that's given us the time to compound our technical advantage and to build out our fully vertically integrated stack.

As I’ve explained many times, I believe proprietary data is the moat of the 21st century, because having data that no one else has enables you to create an AI that no-one else can. As is the case with Roblox, the future of Snap’s user experience hinges on enabling developers to prompt ontologies into existence. This yields a flywheel via which having more and better data enables the ecosystem in question to deliver an exponentially better experience per dollar invested. Further, different user experience philosophies will naturally create entirely differentiated augmented realities.

Snap CEO Evan Spiegel shared some of Snap’s AR advancements this quarter during the Q2 2025 earnings call:

[Prepared remarks]: We have made AR creation increasingly more accessible with Easy Lens, an AI tool that empowers Lens creators to build a Lens in just minutes by typing out a prompt for the Lens that they want to create.

[…]

[Prepared remarks]: Additionally, our new automated speech recognition API supports real-time transcription across dozens of languages and the Snap 3D API empowers developers to generate 3D objects on the fly from any prompt.

[…]

[Q&A section]: And I think as we look forward to the types of experiences people will be able to have with AR glasses, I think we're quickly moving to a world where those sorts of experiences can be generated on the fly.

And again, that's an opportunity where we think we can really differentiate especially because we have developed the developer tools ourselves in support of this developer ecosystem. Developers can actually plug into these various Lens Studio tools as well and design their own plug-ins.

Snap had an operational mishap in Q2 2025, in which they shipped a change in their advertising platform which “caused some campaigns to clear the auction at substantially reduced prices”. This spooked the market, sending the stock down over 25% on the trading days following the earnings report. Although this incident is not great news, the error has now allegedly been corrected and Snap now seems to be positioned for an inflection point over the medium term, following the release of Sponsored Snaps in late 2024. Sponsored Snaps promise to yield improved unit economics and unlock additional inventory, as Spiegel explained during the Q2 2025 earnings call:

And we've been seeing some really great engagement from users as well. So after opening a Sponsored Snap from the chat feed, users exhibit significantly higher engagement per full screen ad view. Driving a 2x increase in conversion, a 5x increase in click to convert ratios and a 2x increase in website dwell times compared to other inventories.

So I think the early signs are very positive. Of course, this is a profound shift in terms of available inventory on the service.

Spiegel doesn’t exude the type of leadership qualities that have historically resonated with me in the past - for some reason, I don’t perceive true customer obsession. However, neither did Lemonade CEO Dan Schreiber and as I explain in my Lemonade Q2 2025 earnings digest, fundamentals are advancing wonderfully since Q1 2025. Despite the narratives surrounding Snap, Snap’s fundamentals are advancing well and the company is making the adequate investments to create long term shareholder value. While I don’t have a conviction with Snap just yet, I will continue watching the company closely.

Until next time!

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc

SNAP is a non starter for me because Class A public shares are practically non voting, and founders control 99% of votes through Class C shares. This means the board has no teeth, and founders face no real pressure from the board or shareholders, except through stock price.

Founder authoritarianism works well only if they stay sane and focused, but that’s a structural flaw. It’s a public company in name only, acting like a private one.

This fails the smell test and it is a red flag in governance. It might work out if founders execute perfectly, but it defies sound investment principles and risk management. Sure, founders can ignore short term noise for long term focus, but with zero shareholder accountability?.

Even the goats Zuckerberg, Bezos, Sergy brin, Larry Page, Larry ellison, Elon Musk have far more accountability to their sharebolders.