Hims Has More Than 100X Potential.

Q1 2025 ER Digest

Hims management is putting the company in a better position every quarter.

My $2,000/share intrinsic value target by the year 2030 may fall short.

Hims’s financial performance is elegantly summarised by its free cash flow production, which is up 321% YoY as depicted below. However, the long term opportunity for shareholders is much larger than the financials currently reflect. Hims is building the infrastructure to leverage precision medicine at scale and thus create a new healthcare industry with an entirely novel objective function: preventing illness. This is the dynamic that I believe takes Hims to a trillion dollar market cap over the coming decade.

60% of Hims subscribers are now utilising some form of a personalised subscription plan. When this metric hits ~100%, Hims will have the infrastructure in place to deliver any treatment permutation to any of its subscribers. Once it has the intel to figure out exactly what is happening inside the body of each subscriber, Hims will be able to deliver precision medicine at scale, affordably and conveniently. I believe this will be a “singularity” kind of moment in the healthcare industry, after which healthcare will never be the same again.

Not-dying-as-a-service is a much bigger business than going to the doctor here and there. And the former format gets more effective as we have more longitudinal health data (for which Hims is excellently positioned to harvest) and AI models get better.

Revenue grew 111% YoY and 30% YoY ex-GLP1. The weight loss segment has dramatically accelerated Hims’s revenue growth and is currently dampening margins. Gross margins are down ~3% QoQ since the weight loss vertical is not accretive to margins at present: according to management, this is typical of verticals that are in their earlier stages. Although the deal with Novo greatly de-risks the GLP-1 operation, I believe the latter will not be the last exponentially growing vertical Hims enters.

As explained by Andrew in the Q1 2025 earnings call, the at home full body testing company was the missing piece for Hims to start to embrace personalised medicine. I believe that we will see new verticals emerge over the coming few years, with similar growth profiles as GLP-1/weight loss - starting with menopause and testosterone:

When we look towards the future, it's clear we are just getting started on the realm of what's possible within healthcare. In addition to evolving our existing specialties, we plan to unlock value for customers in new ways later this year. Earlier this year, we acquired an innovative at home lab testing provider.

As we integrate those capabilities into our platform, we are excited to make blood testing easier and more accessible, giving customers access to testing for key biomarkers tied to heart, hormone, liver, thyroid and prostate health.

These tools will support our current specialties and unlock entirely new ones.

[…]

This lower friction approach to diagnostics is especially important as we expand into hormone driven conditions like low testosterone and menopause. There are over 50 million people in The United States navigating symptoms tied to these conditions and many of them are already on our platform.

Further, Hims’s moat is getting meaningfully stronger as of Q1 2025. Much like Amazon, Hims gets harder to replicate as the frequency of network goes up. The percentage of sexual health subscribers utilising a daily offering came in at 40% in Q1 2025, which is up ~2X YoY. Daily consumption the business harder to replicate, since it requires delivering better patient outcomes with tighter logistical requirements. Additionally, Hims management also shared in the call that these consumers have a 10% better retention in the first year than those not consuming daily offerings.

This dynamic increases the lifetime value of sexual health consumers. It evolves the business from an on-demand and sporadic consumption plane to a stickier format. Applied to the rest of Hims’s verticals, this promises to make the business more profitable and harder to disrupt. Fundamentally, however, this is a continued demonstration of management’s ability to solve a growing volume of acute customer pains, in a way that’s increasingly harder to replicate.

The deal with Novo is borderline miraculous, but perhaps not so much of a management team that has been able to print cash outside of the traditional insurance system for the first time in history - while building all the components of the required vertical infrastructure on the go. Hims wasn’t pointing at the kind of opportunity that I outline at the start of this write up when I first invested, but it doesn’t surprise me either that management has made the right moves to get Hims in this position.

Betting on world class management teams makes you lucky - and doing so early likely makes you wealthy.

A further demonstration of extraordinary management has been the rising operating leverage, in the face of declining gross margins and face ripping growth. As you can see in the graph below, the four buckets of expenses are down considerably YoY as a percentage of revenue. As I outline in my original Hims thesis, they have a considerable dependency on paid marketing which is now decreasing. According to management, marketing leverage was driven by:

More personalisation and a shift towards premium offerings in the sexual health vertical.

A higher efficiency bar for marketing investments. Allegedly, this gave them the wiggle room to launch the Super Bowl campaign.

Organic traffic is picking up.

The latter point is especially important, because Hims has achieved the lion’s share of its present financial performance without word-of-mouth. As it goes beyond stigmatised verticals, Hims is something subscribers are increasingly willing to tell others about. As Hims treats a growing volume of conditions, the relevance of its platform goes up too for a broader demographic segment over time. Therefore, Hims has plenty of upside ahead from organic traffic continuing to pick up.

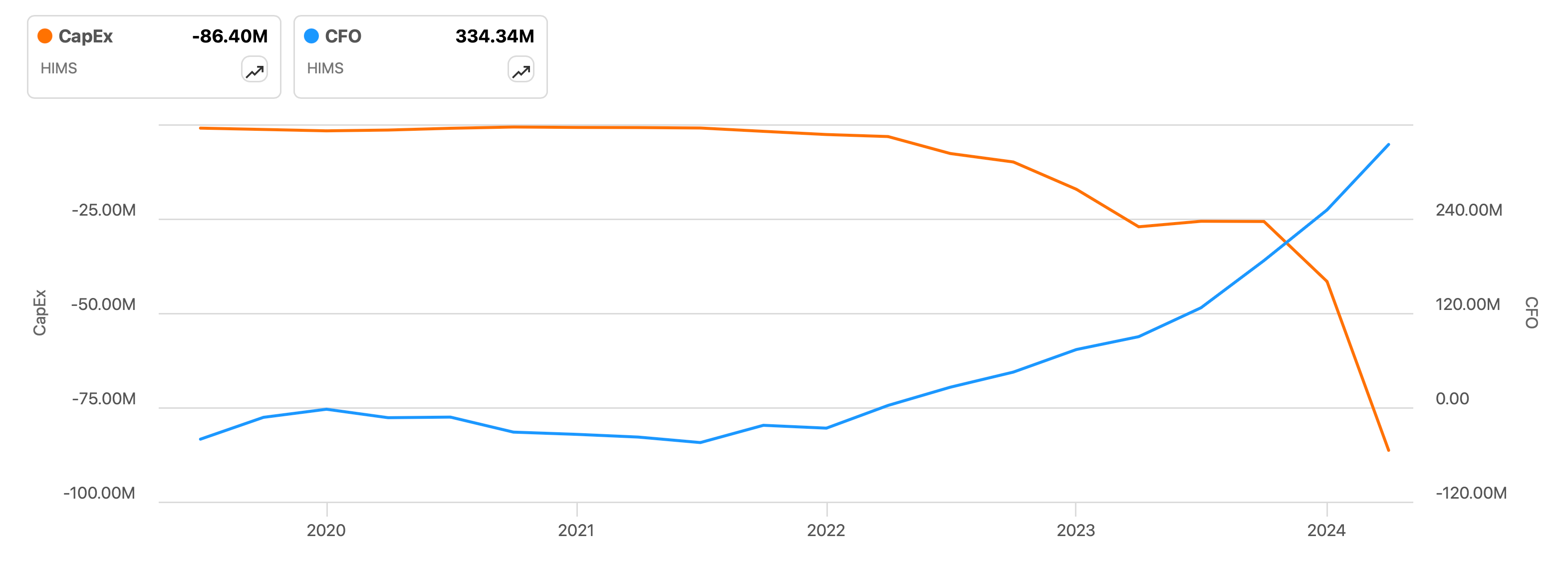

The odds of Hims becoming a much bigger and stronger company continue to increase as CapEx goes up. Cash from operations (blue line, right axis) has risen spectacularly over the past two years, but even more dramatic is the increase in CapEx (orange line, left axis). In essence, Hims continues to reinvest a growing volume of capital into giving customers better deals. As Costco, Amazon, Netflix and Spotify show, this sort of dynamic tends to amount into exponentially larger businesses over the long term.

CapEx came in at $59M in Q1 2025 and was directed towards the following endeavours:

Expanded personalisation capabilities.

The leasing of an additional 400,000 square foot fulfilment facility in Arizona.

Expanded automation capabilities.

Hims CFO Yemi Okupe’s remarks about these investments were highly insightful:

While we are still early in our journey, automation provides a path to unlocking thousands of choices for our subscribers in an efficient manner.

We upgraded equipment in the first quarter across several of our facilities, further enabling us to make the vision of precision medicine a reality. Finally, we invested in infrastructure to unlock sterile fulfillment capacity across our facilities.

This provides a platform for more efficient fulfillment of specialties we are in today, such as weight, and those that we expect to be in the future, such as low testosterone, that require sterile capabilities.

Amazon’s business is about advancing three key pillars forward: price, convenience and selection. Hims is doing exactly the same but with a laser focus on healthcare. The execution remains extraordinary and at a price to sales ratio of just over six, I believe Hims has great upside ahead just from the valuation multiple expansion. Additionally, Hims stands to exponentiate its earning power by more effectively addressing a growing volume of healthcare conditions at a price that the market will be increasingly unable to match.

Until next time and stay focused on the fundamentals!

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc

Congrats, nice article as usual.

I'd like to know your thoughts about the quality of the service reported by end-users on Trustpilot:

https://www.trustpilot.com/review/hims.com

Many customers don't seem very happy about the service received with the subscription model of HIMs.

Isn't this a yellow flag?

Thanks.

"When this metric hits ~100%, "

Why would you assume that? There's no way every subscriber would think of getting a personalised product. I can think of many reasons not to. Many subscribers know exactly what they want and have no need to personalized subscriptions.