Hims: Data Wins.

Q1 2026 ER

Whoever owns biomarkers owns healthcare.

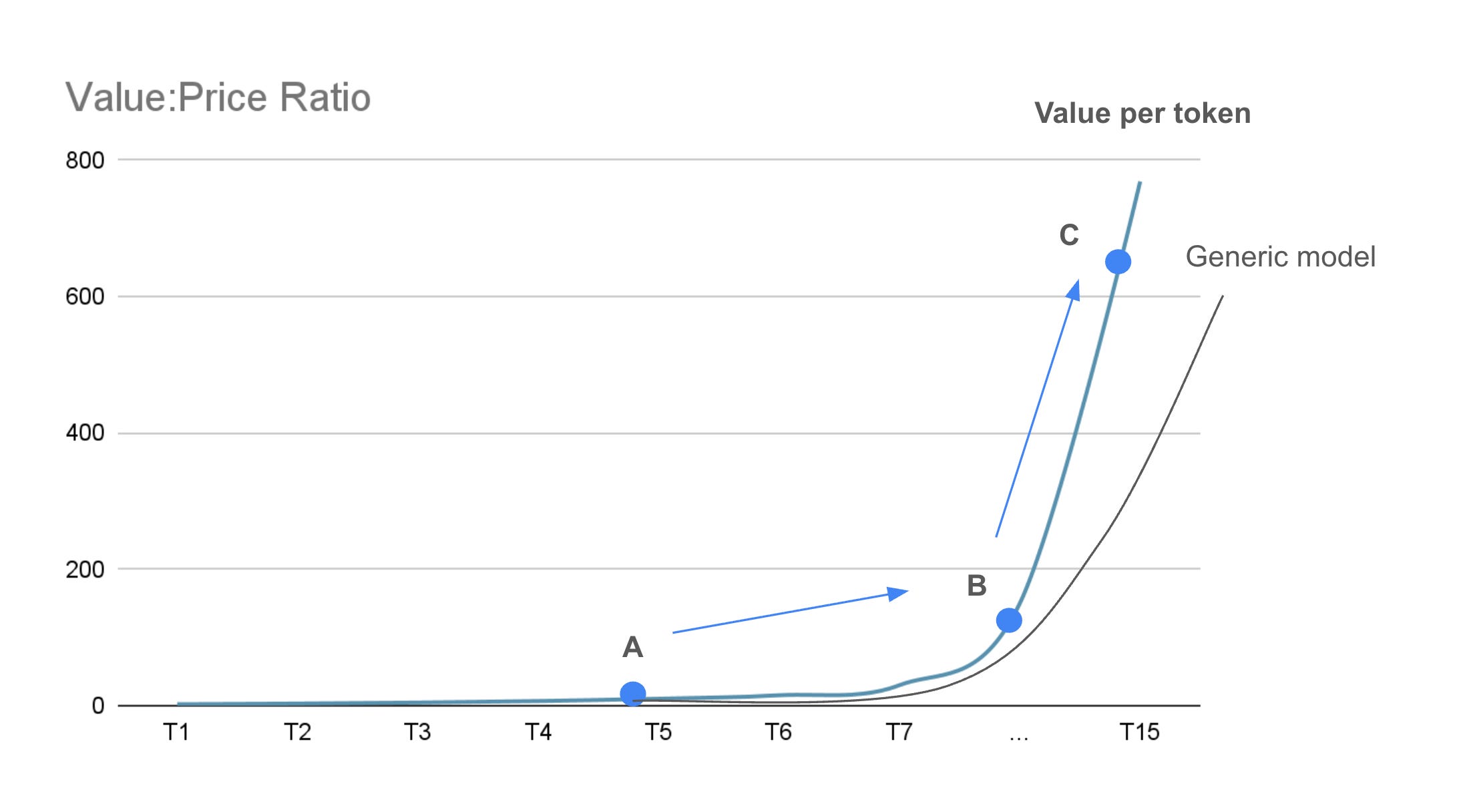

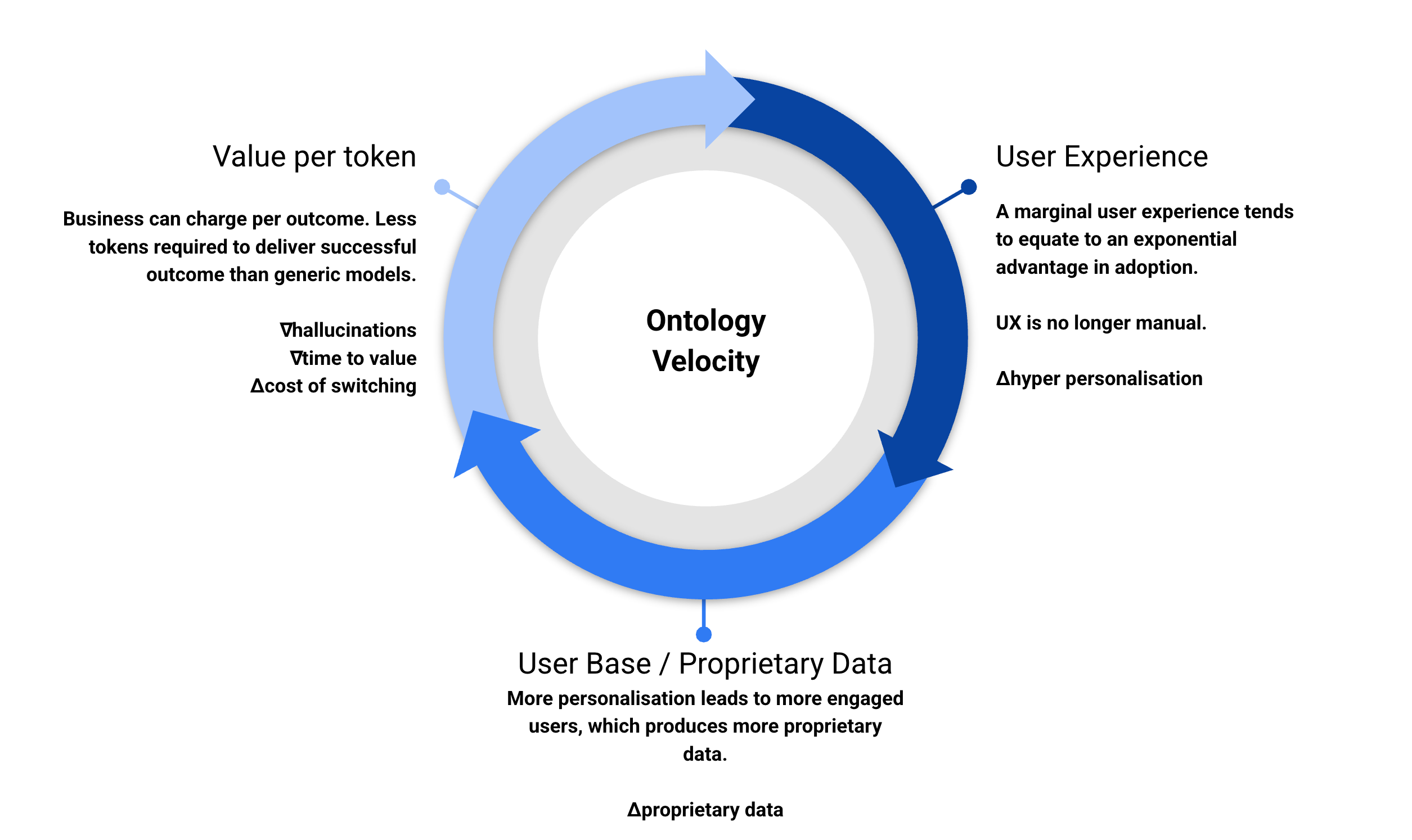

A company can outgrow its prior financial mould without outgrowing its value creation process. Hims has done this in Q1 2026 by becoming a two side operating system. The company’s previous financial model was total pills sold and now it’s total tokens delivered, as Hims becomes the intelligence layer that connects supply and demand in the healthcare system. To maximise free cash flow per share, Hims has to prioritise proprietary data over short term profits in order to deliver more value per token than generic AI models.

Claude is pretty good at delivering healthcare insights if you throw your biomarkers at it. The long term business opportunity is building an infrastructure that harvests biomarkers at a level of scale and quality that others cannot. At the network level, this is what allows you to train whatever frontier model to generate superior insights and deliver more value per token. More patients and more biomarkers than anyone means your proprietary AI becomes biologically more predictive. Long term, this is how you build the healthcare AI that front runs every other AI.

This puts you in a dominant distribution position because customers don’t care about second best, especially when it’s a matter of life or death. This is where the ability to charge extra per token stems from and thus, the new financial model is:

Number of tokens.

Multiplied by net margin per token.

This will serve as the best proxy for Hims’s free cash flow per share over the next decade, rising exponentially as both demand and supply lean ever deeper into the intelligence layer. The moat is the increasing difficulty of replicating the physical infrastructure required to bootstrap the biomarker Ontology, a barrier that compounds every quarter. And it compounds further still because the signals extracted from the physical layer feed directly back into making that same infrastructure bigger, better and harder to replicate.

Over time this flywheel will spin faster and faster. The more biomarkers the network produces, the faster the physical infrastructure evolves, printing even more and better biomarkers in return. This is not a quarterly play. It is a multi-trillion dollar, multi-decade wealth creation event.

Ontology Velocity is the single most important metric for Hims.

Investors have spent a great deal of time and energy focused on short term GLP-1 dynamics. As a subset of peptides, ex-legal dynamics which I dare not model, we will tend to see this part of the operation as a structurally deflationary one. As bio/acc goes mainstream, this will tend to be true for any healthcare offering. However, the pricing power of superior tokens will rise over time. Value is accruing to the network.

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc

Excelente!!

The token economy framing for Hims is the most intellectually honest reframe I’ve seen post-Q1. Most investors are still debating GLP-1 margin compression when the real question is: what’s the pricing power of a biomarker-trained token versus a generic LLM healthcare query?

The moat here isn’t the drug. It’s the ontology — and ontologies compound in ways that balance sheets don’t capture yet.

At Blended Edge we think about healthcare AI through the same lens we apply to semiconductor infrastructure: whoever owns the physical layer that feeds the intelligence layer wins long term. Hims is quietly building exactly that.

Ontology Velocity is now on our watchlist