PBMs Like Cigna are Hims's Life Force

Cigna's New Deal with Lily and Novo

Cigna announced a new deal today with Eli Lilly and Novo Nordisk to offer their respective weight loss drugs at a capped price.

Cigna is the fourth largest PBM (pharma benefit manager) in the US and although the deal looks disruptive to Hims, it’s unlikely to be so in the aggregate. In fact, PBMs are making Hims more competitive every day.

PBMs like Cigna manage prescription drug benefits by negotiating prices and formularies between drugmakers, insurers, and pharmacies, often profiting from the system’s complexity and inflationary tendency. By inflating the prices of drugs in the aggregate, PBMs ultimately make make more money. As I explain in this post, Lily and Novo are on a race-to-scale on the GLP-1 front, because their respective drugs are relatively undifferentiated. This deal is a concession from Cigna in order to maximise GLP-1 distribution for Lily and Novo, that Cigna will nonetheless make up for by inflating prices of other medications.

This is the essence of the US healthcare industry, as I explain in my original Hims deep dive. The US healthcare industry is a monopsony in that there is only one buyer (insurance companies) and therefore demand is relatively inelastic. Providers can increase prices yearly because they will be amortised across a large number of insurees. PBMs may make concessions here and there, but ultimately their business is primarily about driving the price of drugs up so they can take bigger commissions from the industry’s stakeholders. This is why, in aggregate, the move is likely to be scarcely disruptive to Hims, as the latter continues to deploy and grow more verticals below copay.

Indeed, Hims is not a GLP-1 company. It’s a healthcare platform that solves a growing volume of acute customers pains per dollar spent on their behalf, in a way that’s increasingly harder to imitate profitably. Further, Hims management (which has scarcely ever missed guidance) has guided for $750M of weight loss revenue in 2025 with the vast majority of that revenue expected to come for the oral solution and liraglutide (a generic GLP-1). Both of these products are far cheaper than Wegovy and specifically, Hims management estimates their oral weight loss solution is 2/3 as effective as injected analogues and around 1/3 the price.

Thus, whatever the rest of the weight loss industry does, Hims’s weight loss business is well positioned to continue growing fast. In turn, the Cigna deal confirms my view that both Lily and Novo are on a race-to-scale, which increases the odds of Lily signing a deal with Hims, as Novo has done. The Novo deal has considerably de-risked the Hims thesis and a subsequent Lily deal would de-risk it further. Finally, per their incentives, PBMs are set to continue inflating the healthcare market in order to make more money. Ultimately, as Hims continues to deploy more verticals, they will be able to solve problems for patients at a cost that the rest of the industry that revolves around PBMs could not possibly.

GLP-1s are driving much of Hims’s financial outperformance since the weight loss business was launched, which makes the stock price sensitive to GLP-1 narratives. However, GLP-1s are merely on of thousands of types of peptides found in the body with miraculous properties. With the recent acquisition of a peptide manufacturing facility, Hims is positioned to bring many of these peptides to the market. And as the platform continues to compound (increase personalisation, scale and efficiency), Hims will solve patient problems at a level of cost efficiency that will be increasingly harder to copy.

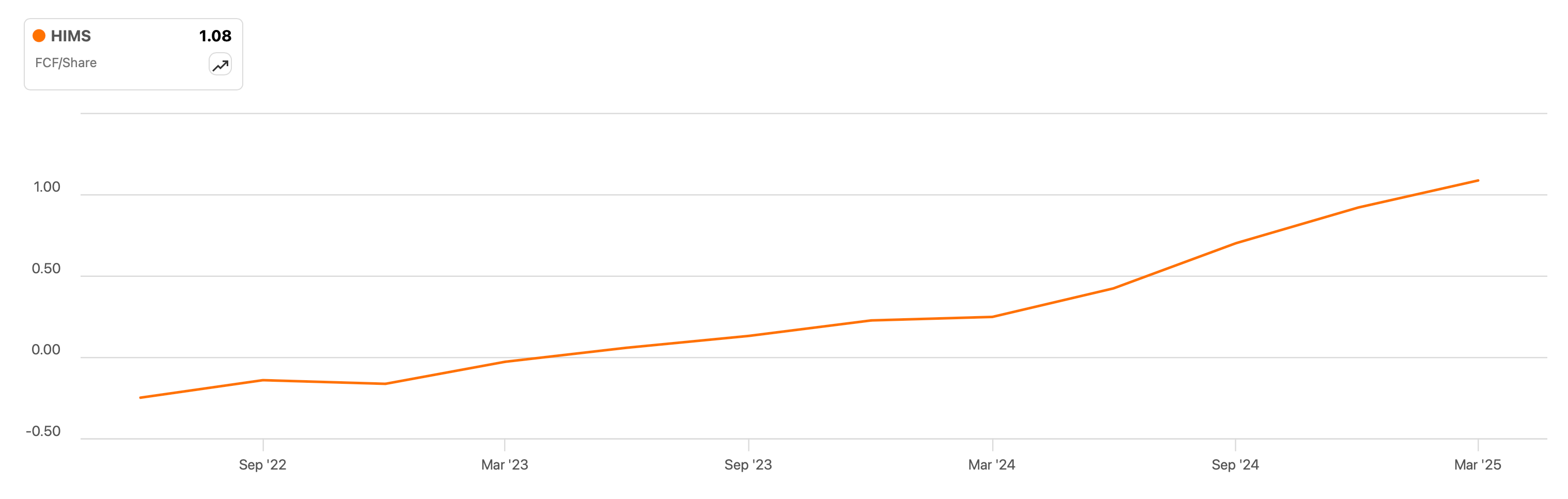

While the market continues to create new narratives about Hims, the latter continues to compound free cash flow per share, which is ultimately what drives stock prices up. This is driven by management’s extraordinary ability to allocate capital and by the compounding efficiency of Hims’s platform. The market insists in looking at Hims mono-dimensionally, but this is a platform with endless optionality. Focusing on GLP-1s now when analysing Hims is like focusing on the Harry Potter books when analysing Amazon back in the early 2000s. Further, I believe that with the onset of precision medicine, Hims is currently building the most valuable subscription service on Earth.

Until next time!

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc