Palantir and Hims Earnings Preview.

Update

This is an update of my original Palantir and Hims deep dives.

You can also read my original Microsoft, Amazon, Meta and Nvidia deep dives for free, to get the most value out of this piece.

1.0 Palantir Q1 2025 ER preview.

Meta’s, Microsoft’s, Amazon’s and Nvidia’s latest earnings report show AI continues to scale fast. Which means that Palantir has likely continued to grow exponentially in Q1 2025.

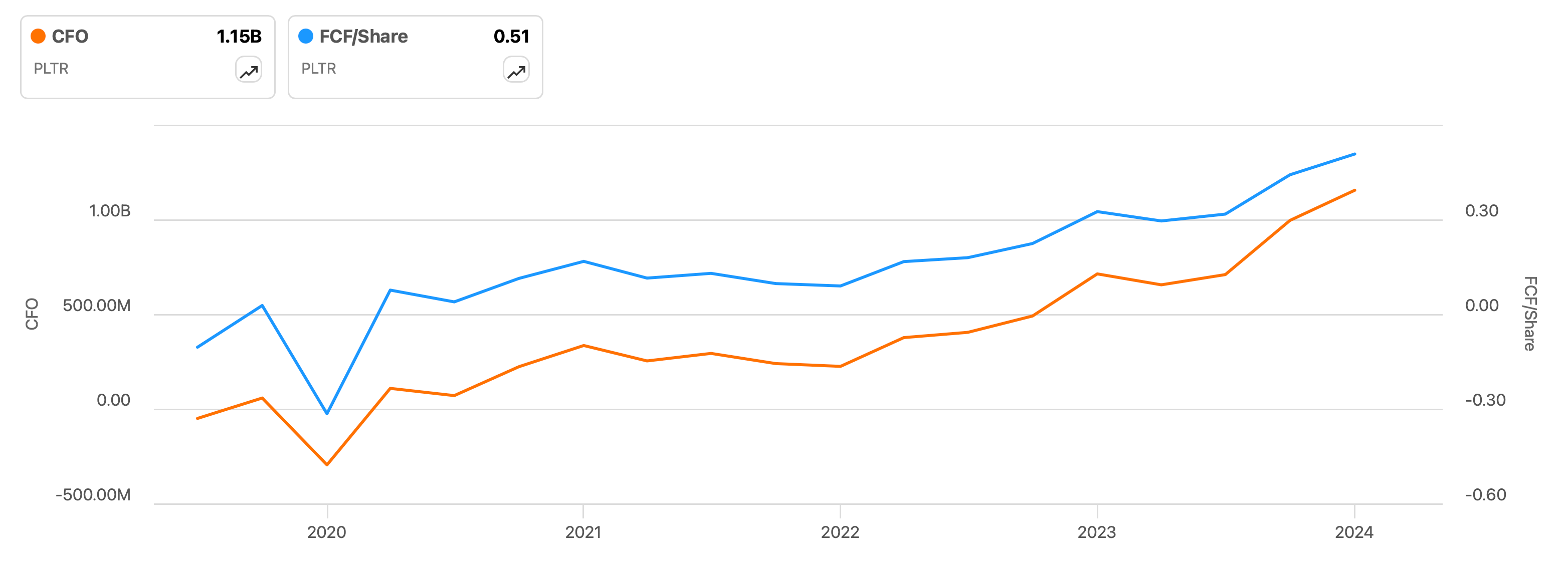

Palantir’s financial performance has thus far been a direct function of the evolution of AI models (as is the case with other Singularity Scalers). As AI models have exponentiated their capability, Palantir has rapidly decreased the time to value for customers and increase the value delivered to customers per dollar spent. As a result and as you can see in the graph below, cash from operations (orange line, left axis) and free cash flow per share (blue line, right axis) have risen non-linearly over the past few years, driving the stock up considerably.

Last week I sent out my Meta Q1 2025 update, showcasing how AI models continue to scale, which is bullish for the Palantir thesis. Amazon’s and Microsoft’s Q1 2025 ER point in the same direction, with the CEOs of both companies essentially saying that they don’t have enough compute power to satisfy both internal and external AI demand. My conclusion having read through both earnings reports is that demand for Palantir’s (AI) software is likely to have accelerated meaningfully quarter over quarter.

Here’s the key data from Microsoft’s latest earnings report that suggests demand for AI continues to accelerate. According to Satya:

Model capabilities are doubling in performance every six months, thanks to multiple compounding scaling laws.

Microsoft’s cost per token has halved over the last year.

Github Copilot users are up 4X YoY (the AI Agent that automates coding).

Microsoft 365 Copilot users are up 3X YoY (the AI Agent that automates office work).

Tokens processed via Microsoft’s Foundry (Palantir Foundry’s pseudo-knockoff) are up 5X YoY.

Microsoft is now introducing vertical AI Agents for every role and business process. Custom agent creation is up 130% QoQ.

Especially interesting is the last point, that suggests verticalized AI agents are taking off. You may remember that I’ve been talking about verticalized operating systems and AI agents promising to take Palantir’s valuation much higher than today’s, by enabling the creation of autonomous organisations. Incidentally, Palantir’s stock price recently began a recovery back to ATHs after Palantir announced they are working on AI FDEs (AI forward deployed engineers) - which are a form of verticalized AI agents and promise to enable Palantir to get exponentially better at deploying its software (thus growing faster).

My view is that absent any operational anomalies, Palantir’s earnings tonight should reflect continued productisation and thus higher growth rates and margins in its US commercial business, or at least clear visibility for such evolution going into the next few quarters. Qualitatively, Palantir now enables folks to take AIP Bootcamps anywhere and any time and this alone should yield improved financials this quarter.

Amazon’s Q1 2025 earnings report showed customers increasing the frequency with which they shop everyday essentials (growing twice as fast as the rest of the retail business, which as explained in this post, stands to make Amazon’s moat much stronger over the coming five years. However, the real standout for Palantir’s Q1 2025 ER is Jassy’s qualitative remarks about the current state of AI supply and demand:

And I would tell you that our AI business right now is a multi-billion dollar annual run rate business that's growing triple-digit percentages year-over-year.

And we, as fast as we actually put the capacity in, it's being consumed. So, I think we could be driving -- we could be helping more customers and driving more revenue for the business if we had more capacity.

And some of that is just because there is so much demand right now, but I do believe that the supply chain issues and the capacity issues will continue to get better as the year proceeds.

Jassy’s remarks are a match with the above quantitative nuggets from Microsoft’s Q1 2025 earnings report. Together with the last Meta and Nvidia earnings reports, the magnificent seven proves the broader AI thesis continues to evolve successfully, which makes it more likely than not that Palantir keeps up with (or continues to accelerate) the growth rates seen last quarter.

2.0 Hims Q1 2025 ER preview.

The Hims and Novo deal is likely to kick off a chain reaction in the pharma industry, in which Hims takes on a role similar to that of Spotify in the music industry.

The market has started to price in the drastic reduction of Hims’s legal risk. And this process may accelerate if Andrew gives us more information about the “roadmap” with Novo the deal comprises.

Hims’s FY2025 revenue guidance included zero commercial GLP-1 revenue guidance and that is set to change in tonight’s call, with the Wegovy deal that was recently signed with Novo Nordisk. Digging into Novo’s Q4 2024 earnings call transcript, it is apparent to me that they’re on a race-to-scale with Lily on the GLP-1 front. Because their respective products are relatively undifferentiated, both companies want to achieve the maximum scale in order to capture the market’s loyalty via brand recognition.

If this interpretation of mine is correct, it means that the Hims <> Novo deal is likely to kick off a chain reaction in the pharma industry. I believe this is likely because in Q4 2024 Novo sacrificed short term financial performance in order to maximise scale, showing that their top priority is actually scaling faster than competitors. See Novo VP of US Operations David Moore’s remarks, during the Q4 2024 earnings call:

Wegovy sales increased by 86% globally, driven by a 59% growth in North America operations, and Wegovy sales in International operations have reached more than DKK 11 billion. The global total branded obesity market more than doubled with a growth rate of 119%.

In the U.S., the Wegovy sales growth was driven by increased volumes, partially countered by lower realized prices in the U.S.

Novo CFO Karsten Munk then clarified what drove the lower realised Wegovy prices:

In North America operations, the cost increase is mainly driven by promotional activities related to Wegovy.

In International operations, the increase is mainly related to obesity care market development activities, Wegovy launch activities as well as promotional activities for GLP-1 diabetes products.

In the Q&A section of the call, David Moore then clarified that Novo’s focus is driving new prescriptions (or scale, in other words):

Driving new prescriptions is, of course, our focus. And what we can say about that is we are shipping more of the starter doses as we speak.

Novo’s financials are doing just fine, which means the deal is likely not the result of the pursuit of short term financial performance. Although revenue (orange line, left axis) and cash from operations (blue line, right axis) are down QoQ, this is due to seasonal readjustments of prescriptions in Q1, with Novo’s sales being up 25% YoY. Indeed, the deal seems to match the strategy that Novo management outlined in the Q4 2024 earnings call: maximising scale, even if at the expense of short term financial performance.

Meanwhile, Lily CEO David Ricks sounded a little bit sour in his last interview with Yahoo Finance:

We're not interested in exclusive deals. We think innovation and choice is very important. And we're well into the product replacement cycle, and there's more coming.

[The Hims and Novo deal] is in some ways a little disappointing to see this. It feels a little bit like last decade, these sort of lock-up deals.

The deal with Novo also reduce Hims’s legal risk dramatically, effectively neutralising the until-now prevailing bear thesis. At a price to sales ratio of around 6.5, the market has started to price in the reduction of this risk. In turn, the risk is further mitigated by the long-term component of the Hims and Novo deal. The latter is not only about Hims distributing Wegovy via its platform, but as David Moore said in the official press release, it’s also about the two companies executing on a long term roadmap together:

We are pleased that Hims & Hers is making this offering available this week to people living with obesity.

Beyond this initial collaboration, the companies are developing a roadmap that combines Novo Nordisk’s innovative medications with Hims & Hers’ ability to deliver access to quality care at scale, with the goal of improving long-term outcomes for more people living with chronic disease, and doing that more affordably.

Novo has seemingly figured out that their business is about beating Lily in the race to capture the top-of-mind spot for innovative, effective and safe weight loss drugs (and other categories as they continue to look deeper into the peptide space in my view). And that therefore, maximising the distribution of their ideally leading portfolio is their primary strategic goal. I believe it won’t take Lily long to figure this out too.

Additionally, I expect Hims to continue growing their subscriber base in Q1 2025 and have visibility into the launch of new verticals, based on the recent acquisitions of the at-home full body testing company and the peptide manufacturing facility.

Best of luck tonight, Palantir and Hims longs! And remember - although the build up to the earnings reports tonight is fun, remember that a quarter rarely makes or breaks a company. Indeed, investors mentally handicap themselves with big expectations for earnings. The market tends to react hysterically in any direction, but good fundamentals are subtle. What matter is free cash flow per share rising sustainably over the decades from current levels and that is often a far more silent and discrete process than the quarterly circus.

Until next time!

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc