I’ve switched up my style on Youtube, riffing my raw thoughts on camera rather than reading my write ups. Scripted content will stay around, but for now you guys are loving this format on Youtube and so I’ll keep on doing it!

Edited by Brian Birnbaum and an update of my original HelloFresh deep dive.

HelloFresh is increasingly in a position to take the entire market, as it makes its highly complex and uncontested infrastructure profitable.

HelloFresh’s unit economics continue to improve, as evidenced by the rising free cash flow per share depicted below. Marketing expenses as a % of revenue were down 310 basis points (bps) YoY, as HelloFresh continues to focus on acquiring less but more profitable customers. AEBITDA margins for the meal kit and ready-to-eat segments hit records of 14% and 5% in Q4 2024, coming up from 8.5% and (0.1)% in H1 2023, respectively.

HelloFresh is therefore positioned to potentially take the whole market. And price at 0.18 times sales, the situation is increasingly asymmetric.

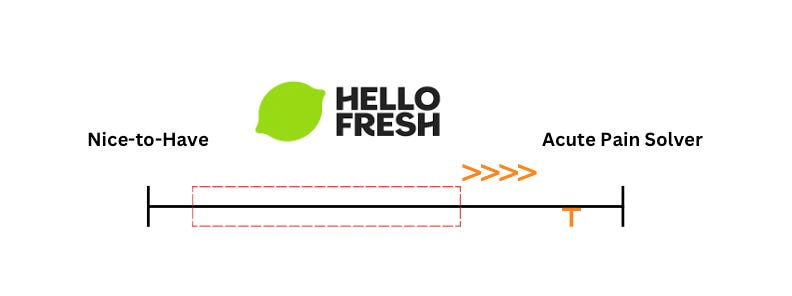

As I explain in my original deep dive, HelloFresh operates one of the more complex supply chains on Earth, bringing fresh food on demand (cooked or ready to be cooked) to millions of people worldwide. When I first studied the company in July 2024, they were more nice-to-have than must. By focusing their marketing efforts on customers that value time over money, they are now gradually beginning to resolve acute customer pains. The shift is increasing the profitability of their highly complex infrastructure.

HelloFresh seems to have no competition. The rest of the players are vertical, without a platform that enables them to launch subsequent verticals at a marginal cost like HelloFresh. The result of taking the whole market and becoming an acute pain-solver is better unit economics, which affords greater reinvestment, potentially kicking off a powerful flywheel from there.

Meanwhile, as CEO Dominik Rikter explained in the last earnings call, HelloFresh is already making progress with new verticals that could further improve the profitability of their platform:

In addition, we've also made good progress in further diversifying our TAM and revenues with our still early stage forays into pet food, premium butchery services and most recently, into health supplements.

In essence, the HelloFresh thesis is the same as Spotify’s: they’re building a platform that may later on enable them to launch additional verticals at will, increasing average revenue per user exponentially.

HelloFresh’s ability to optimize complex processes is clear, evidenced by the stable cash from operations. The meal kit segment has been declining post-pandemic, with people resuming normal eating habits. Despite this decline and the enormous complexity of the supply chain, HelloFresh’s cash from operations remains positive. For this reason, I believe that HelloFresh is more likely than not to continue increasing margins and eventually become a much more profitable company.

In 2024 meal kit revenue declined 9%, while RTE (ready-to-eat) revenue increased 40%. Given the much larger size of the meal kit business, total revenue only grew 0.9% in constant currency terms in 2024. Managing the rapid growth of the RTE business is probably even more complex than managing the decline of the meal kit business. By managing the two simultaneously, HelloFresh is managing extreme complexity while producing cash.

For this reason, I am increasingly confident in HelloFresh’s ability to manage verticals. I believe it’s likely that they deploy more verticals successfully, which ultimately drives free cash flow per share. Since I don’t understand HelloFresh’s customer, I don’t know where the bottom is for the meal kit operation or exactly how much potential the RTE business has. However, I am now fairly certain that HelloFresh is led by a world class management team.

The focus for HelloFresh in 2025 is efficiency, with management guiding for a further 10% decline in the meal kit business and “only” mid-teen percentage growth for the RTE operation. I believe the HelloFresh thesis will be much clearer going into 2027, once it’s achieved greater efficiency and returns to growth.

By H1 2027, I think it’s likely that HelloFresh sees a significant increase in cash flow, along with clear growth drivers. At the moment I don’t have clarity on the latter, which is why I continue to monitor the company quarterly. At present I’m not a customer of this sort of service, so I struggle to understand who would like to use it and why.

Until next time!

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment.

You can also reach me at:

Twitter: @alc2022

LinkedIn: antoniolinaresc

Hi can you do a follow up on HelloFresh's Q125 earnings? Thank you